Last year, after Deb Jerikovsky's husband died, she decided to swap the lake home where they planned to spend retirement for a house in the metro that's closer to family.

She put that plan on hold, however, once she realized 7% mortgage rates would force her to dip too deeply into her savings. Instead, she moved in with her daughter, hoping she'd eventually score a lower rate.

She didn't have to wait long.

Mortgage rates were still hovering near 7% last October when she ran across a listing for a townhouse in Coon Rapids that touted a KitchenAid fridge, electronic blinds and an unexpected extravagance: a low-interest assumable mortgage.

"It was like winning the lottery," said Jerikovsky, who assumed the seller's 2.25% mortgage rate.

The deal saved her about $700 a month compared with today's rates and gave her enough room in her budget to buy a new car and spend part of the winter with her aunt in Florida. Her $349,900 townhouse is one of hundreds of listings in the Twin Cities with an assumable mortgage eligible sellers can transfer to qualifying buyers, teleporting them back to a time of record-low rates.

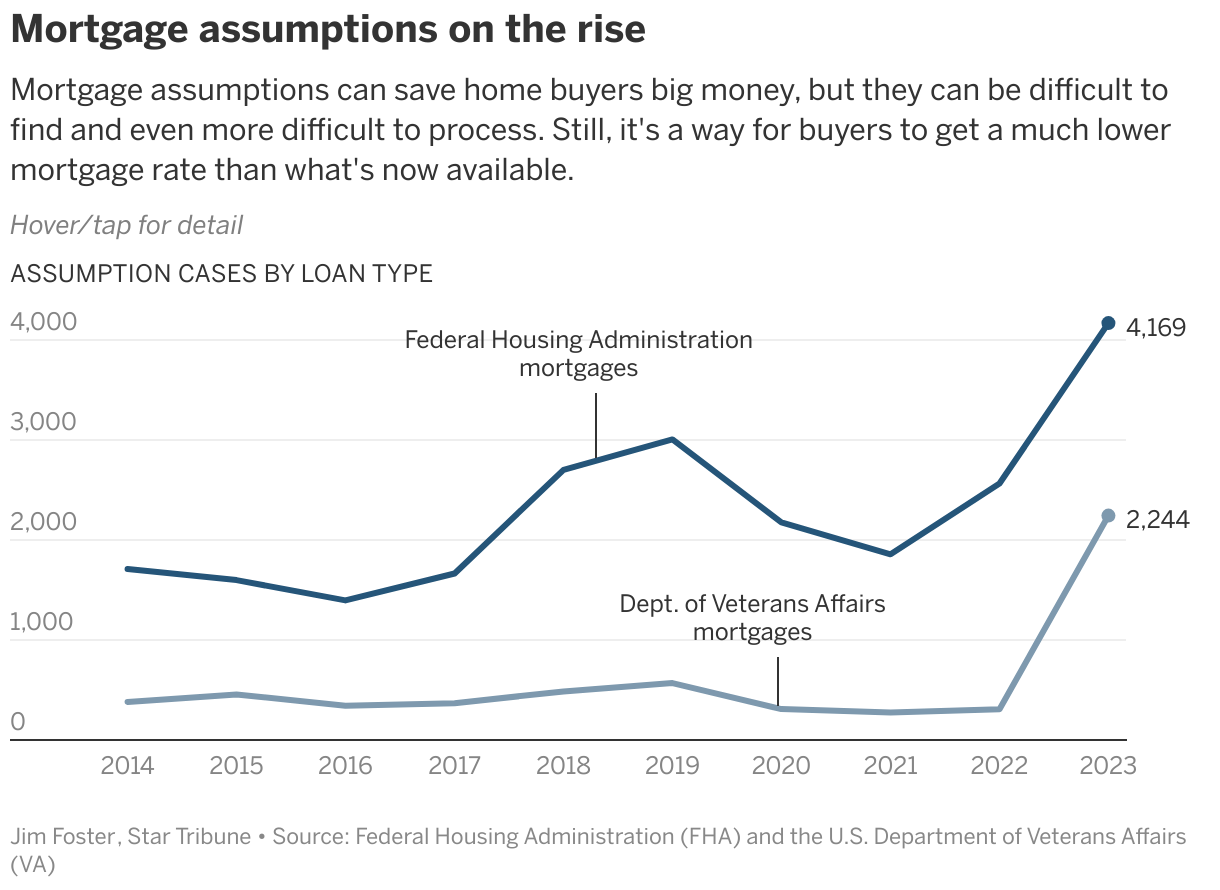

Though they now account for only a fraction of all house listings, these government-backed mortgages — courtesy of the Federal Housing Administration (FHA), Veteran Affairs (VA) and U.S. Department of Agriculture (USDA) — are an overlooked home-buying hack saving a growing number of buyers hundreds of dollars a month and tens of thousands of dollars through the life of their mortgages.

"Most agents aren't even aware of what it entails and what to look for," said Tyler Miller, a local broker who has been involved with several sales involving assumable mortgages with astoundingly low rates.

Miller recently listed a four-bedroom house in Blaine with an assumable 2.25% FHA mortgage with a monthly payment that's about $1,700 less than it would be at the going rate. To tout the listing, he posted a TikTok video promoting the benefits.

"I had some people tell me I was lying," Miller said. "I said, 'No, this is real.'"

Back in vogue

Assumable mortgages have been lurking in the shadows of unusually low rates in recent history. Such mortgages were last popular in the 1980s when rates hit a record 18.1%.

At the end of 2020 and into early January 2021, rates fell to record lows, hovering around 3% for much of 2021 and causing home sales and prices to soar. That buying binge locked in thousands of mortgages at rates that likely won't be that low again for decades. An estimated 80% of all VA mortgages, like the one Jerikovsky assumed, now have a rate that's less than 4%, and many of those rate-holders are now ready to sell.

Today, the average 30-year fixed-rate mortgage is about 7%. Though that's still below historical averages, there's a generation of buyers yearning for a time of low rates that's unlikely to re-emerge anytime soon.

An estimated one-third of all mortgages in the U.S. are assumable now. Because many owners will hold onto those rates as long as possible, assumable mortgage listings represent only a fraction of homes currently for sale, making them one of the best-kept secrets for homebuyers these days.

While some agents will include an assumable mortgage in the listing details, many homeowners don't even know they have one — the details are buried in the fine print of their contract, which many buyers don't carefully read. In Minnesota, just shy of 5% of the more than 30,000 houses listed on Realtor.com had assumable mortgages. The website only started including a search feature for assumable mortgages in February.

Ryan Carrillo and Louis Ortiz started their Assumable.io website, which is dedicated to assumable mortgages, after Carrillo discovered the 2.75% FHA mortgage on his own house was assumable.

The site lets you search for listings city by city, including detailed mortgage data such as the assumable rate and payment compared with the payment at current rates. All of the more than 30,000 nationwide listings on the site have an assumable mortgage, including other key details such as the required down payment and the interest savings through the remaining mortgage.

"It's a huge opportunity," Carrillo said, nothing that traffic to the site has doubled every month since its launch.

Some catches

A recent listing for a nearly new townhouse in Maple Grove initially priced at $485,000 came with an assumable mortgage that's half the current rate, saving a would-be buyer about $1,000 a month. Through the life of the loan, that lower rate would save nearly $400,000 in interest payments.

Roam, which doesn't yet post listings in the Twin Cities, is another new website focused solely on assumable mortgages. It charges buyers 1% of the purchase price to help navigate the process. On average, the company claims, buyers who use the site save $15,000 in mortgage payments annually.

"It's not a panacea and won't work for every transaction and every buyer," Ortiz said. "But it provides buyers the opportunity to afford more house if they can make the equity gap work."

That equity gap is often the biggest hurdle. Because the buyer is essentially taking on the existing mortgage rather than receiving a new one, the buyer has to pay the seller the difference between the original mortgage balance and the current asking price.

Though it's only been a couple years since rates spiked, that equity gap can be significant given how house prices have steadily risen. To eliminate that barrier, Ortiz and Carrillo said they're now offering lenders willing to do a second mortgage access to their site.

Chris Birk — vice president of Veterans United Home Loans, which has a national network of agents who specialize in working with military buyers — said there's been a 600% increase in the number of VA mortgage assumptions from 2022 to 2023.

"We're seeing marked increase interest in these," he said. "But it's a foreign concept for so many buyers but also sellers."

He said while any lender or servicer should be able to complete the transaction, it helps to work with professionals who are familiar with the process.

Brady Holland, the agent who helped Jerikovsky buy her townhouse, said assuming a mortgage can be a bit more complex because both the buyer and seller have to provide documentation. That's especially true for the seller, who is essentially "selling" the mortgage to the buyer.

"It was a little tricky," he said. "I had to call [the processor] every other day to check on things. ... It takes a team to make it happen."

Many VA mortgage holders are reluctant to let another buyer assume their mortgage because once they do, they forfeit the right to use the benefit to buy another one. Unlike FHA mortgatges, VA mortgages are considered a government benefit with perks that include the ability to forgo private mortgage insurance and no, or a low down payment and competitive low rates.

A VA mortgage holder is entitled to transfer those benefits to a qualifying nonveteran, as long as the seller doesn't plan to buy a home with another VA loan.

In the case of the house that Jerikovsky bought, the seller was a widow who moved to an apartment, enabling her to waive her right to additional VA mortgage benefits because she doesn't plan to buy again.

Though a mortgage assumption can take longer than a new, traditional mortgage, that wasn't the case for Jerikovsky's purchase, which closed less than two months after she first saw the house. For her, the most challenging part of the process, she said, was filling out online forms and applications. But her tech-savvy daughter helped with that.

"I didn't know if I would be living with my daughter for six months or a couple years until rates went down," she said. "That [assumable] rate made all the difference in the world."

Delta hiked fares for solo travelers, until Twin Cities travel experts caught the change

In first speech back, UnitedHealth's new CEO pledges to review hot-button issues

A child had measles at Mall of America, concerning state health officials who don't know source

Ramstad: Gov. Walz, things are not getting done in Minnesota