The success of Minnesota's experiment allowing THC consumption in bars, restaurants and taprooms for the past two years has come at a high price: Insurance costs are astronomical, and policies are hard to find.

"It's always fun to be the first to do things, but it comes with a lot of headaches, and we're finding insurance to be that primary hurdle," said Bob Galligan, director of government relations for the Minnesota Craft Brewers Guild.

The main issue is a lack of experience in the industry. Because there haven't been any lawsuits for a business over-serving cannabis to someone who later crashes their car, as an example, insurers aren't sure what their liability might be.

"They don't know how to provide coverage unless something has happened. It's a blessing and a curse at the same time," Galligan said. "Insurance providers want thousands of pages of data to write that policy, but as I tell our members, we are that data."

With alcohol, decades of claims and court cases can pinpoint potential liability based on a tavern's sales and address. Because on-site THC consumption is so new and has so many unanswered questions, policies can cost twice as much for far less coverage compared with liquor liability or "dram shop" coverage.

And the largest insurance carriers typically won't touch cannabis at all because they operate globally and don't want to risk money moving from a place where cannabis is legal to a part of the world where it is not.

"Because these companies are global, they run into money-laundering issues," said Cory Lake, owner of Lake Group Insurance, which handles cannabis policies. "That would be way more expensive than money you'd be winning from any sort of cannabis business."

The issue has turned into a persistent growing pain for the industry in Minnesota and has caused some businesses to keep THC off the menu as insurers deny or don't renew coverage.

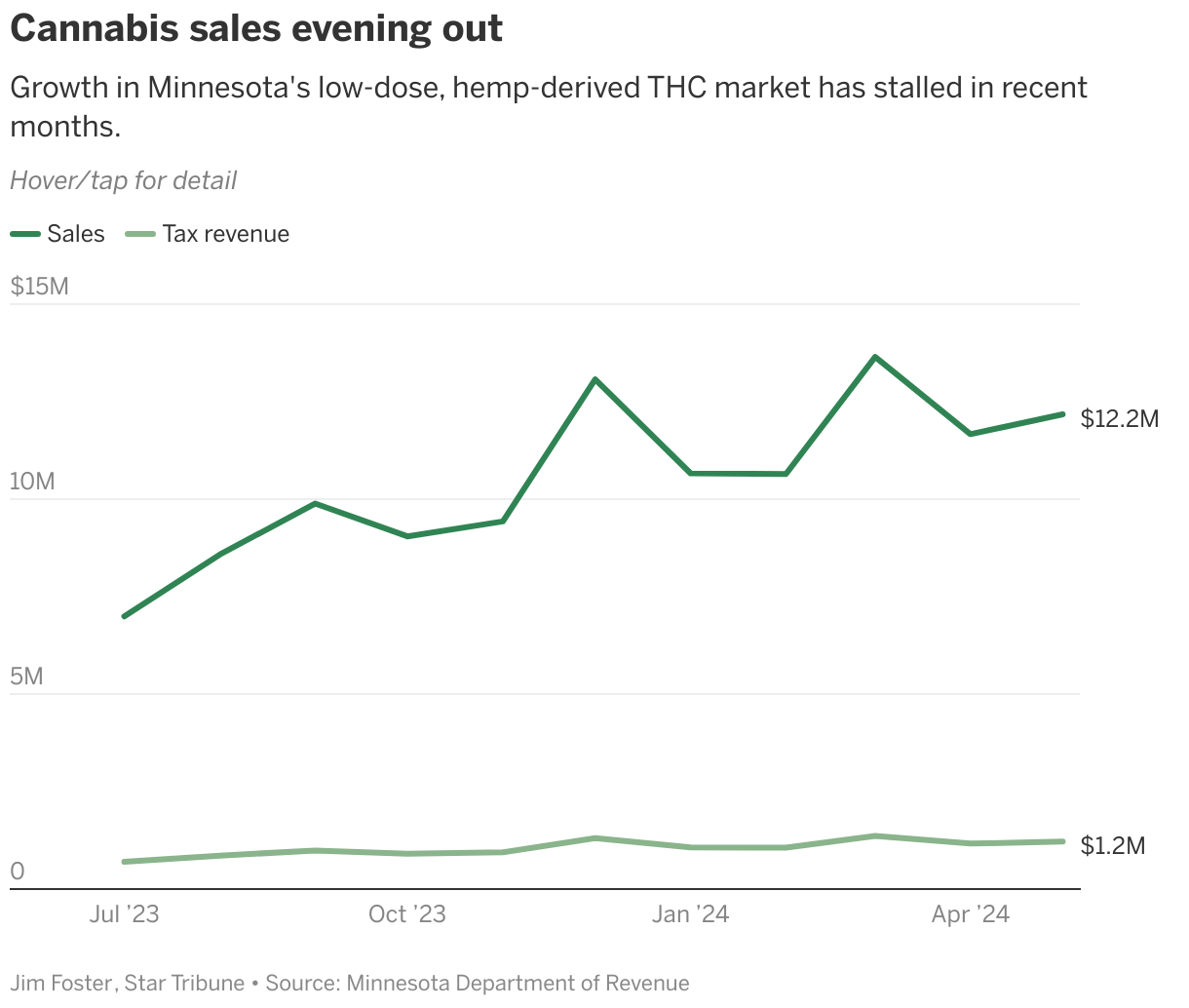

While liquor stores and other retailers would benefit from continued restraints on THC seltzers on tap, monthly cannabis sales have slipped since peaking around $13 million in March, according to preliminary Minnesota Department of Revenue data.

Other than federal policy reforms unlikely to advance out of Congress this year, there are few legislative fixes to address the insurance issue in the short term, experts say. It will likely take years for insurance costs to fall and for policies to become more widely available, though it could happen sooner if more states allow on-site consumption.

"Usually in insurance, it takes 10 to 20 years to really get a grasp on what actual risk profiles look like, and it has to happen on a national level," Lake said. "Minnesota is the only state that's really doing what we're doing."

Even in states that legalized marijuana years ago, cannabis lounges have not reached the same saturation and acceptance as the low-dose market in Minnesota, which allows serving hemp-derived THC beverages and foods on-site at registered outlets.

Among the first was Minneapolis Cider Co., which launched its Trail Magic THC drinks two years ago this month.

Owner Jason Dayton said part of the issue is reinsurance firms, which insure insurance companies, aren't willing to deal with cannabis. As a result, he said, "the cannabis policies that do exist and are available are really expensive."

"It can be $7,000 a year for just $100,000 in coverage," Dayton said. "Contrast that to our alcohol policy: We have $5 million in coverage."

The cidery decided to self-insure against potential cannabis liabilities, which Dayton acknowledged was a fortunate position since it means being able to pay out of pocket.

For smaller businesses that might not have $100,000 on hand to defend a lawsuit, there are options. It might take some shopping around and calling breweries, restaurants or trade groups to see how they made it work.

"Prices of these policies should fall once more data is collected," said Josh Havlik, an agent at Miller-Hartwig Insurance.

"I am unaware of any litigation regarding on-premises sale of THC, meaning that establishments here in Minnesota have been taking their responsibilities to the public seriously. More options are on the horizon as insurers see the opportunity to make a profit."

Restaurants are often able to find ostensibly cannabis-friendly policies, which might not cover THC liability but at least aren't under threat of cancellation because of cannabis sales. And that availability should improve into next year.

With such a policy in hand, Lake Group and other local insurers offer secondary insurance that fills the cannabis liability gap. It's "not inexpensive," Lake said, but he added restaurants should look at THC seltzers as a value beyond the cost per can.

"If people have a couple of beverages, maybe they'll buy more food," he said. "Maybe they'll buy the dessert."

Havlik said it's important for businesses to know their policies and keep alcohol and THC service separated.

"The on-site consumption policies available all have liquor exclusions in them; this creates a risk to any establishment who may serve a patron both by mistake," he said. "I have suggested hand stamping or wristbands, especially during busy times or events."

The insurance question goes beyond neighborhood bars, restaurants and breweries. It extends to bigger venues that could continue bringing THC to the mainstream but aren't selling cannabis products yet because of the unknown liabilities in this new, and profitable, market.

"As you think about the cultural touchstones that build categories and consumer confidence," Dayton said, "it's the State Fair, U.S. Bank Stadium, Target Field, all these larger venues that aren't able to sell these right now."

Brooks: Hard lives led to hard-won diplomas for these Minnesota high schoolers

Trump races to fix a big mistake: DOGE fired too many people

St. Paul sees 'unprecedented' day care closures, sending families scrambling

One man dead in shooting Friday outside Northtown Mall in Blaine